Welcome to the 2022 and 2023 Meldel annual report! Apparently, I release these every two years now because of a general dread of the chore. So why submit myself to this torture? Three reasons. First, I need to have a better understanding of how I make and spend money as an independent designer. Spending time swimming in the business side of my business may not be fun, but financial review is a necessary part of successful self-employment. Second, I sincerely hope my trials, tribulations, successes, and failures are relatable and can help motivate others to take on freelancing. I have learned a lot of lessons about running a business the hard way and hope to share that knowledge. Third, I want to challenge the practice of gatekeeping and salary secrecy. It’s true that most of the folks proselytizing pay transparency are advocating for it in a corporate job setting. But for freelancers, the reasons are often the same—a data point that you can share with others to make sure you are in sync with your professional value. Wannabe freelancers can see what kind of income is realistic, and understand how many projects and clients it takes to get there. That said, my experience and method of freelancing is just one way to be. Last year I outlined four freelance styles based on myself and some close colleagues. Whatever path you’re on, it’s invaluable to share openly with others, to compare rates, and find what is just right for you.

Overview

The years 2022 and 2023 fall neatly in line with my six-year trend of hovering around 100,000 in total income. Whoosh!!! Did you feel that gust of air? That was a huge sigh of relief coming from me. The previous two pandemic years had been very successful for me, mostly because of a major, multi-year public health project that I was a part of through an agency.

This kind of long-term campaign was stabilizing during an unstable time. When the funding went away (and the agency folded), I was worried it might deeply affect my income.

Luckily, this was not the case, and I was able to bring on new clients like Travel Portland, Mt Hood Territory and Columbia Riverkeeper among others. When I look at the numbers, I have about 16 active, regular clients. That brings about 55 projects per year (about four per month). But, if you look at how my income divides up by month, you will see that there are major spikes and dips. So, I may have six projects going on at once one month, and a mere three the next month. I do think I need to increase my client roster by a few in order to stabilize monthly income.

2022 marked my first year teaching at PNCA, in addition to PSU. In general, I am teaching every other term or for about half of the year. While still a small portion of my income, teaching continues to be rewarding for me personally and offers an opportunity to contribute to retirement (see retirement section below) and an opportunity to apply for professional development grants. The grants are a great perk to adjunct teachers. Through these grants I was able to travel to Portugal to attend a Design History Society conference in 2023, and secure money for scanning large-scale, historic design works for my Portland Design History project. You’ll notice that teaching income varies year-to-year, that is because I taught a special “workshop” class in 2022 for PSU that took a group of students to San Francisco. And for PNCA I have earned extra income being a thesis mentor and a very occasional substitute.

S-Corp Onboarding Disasters

(Yes Plural)

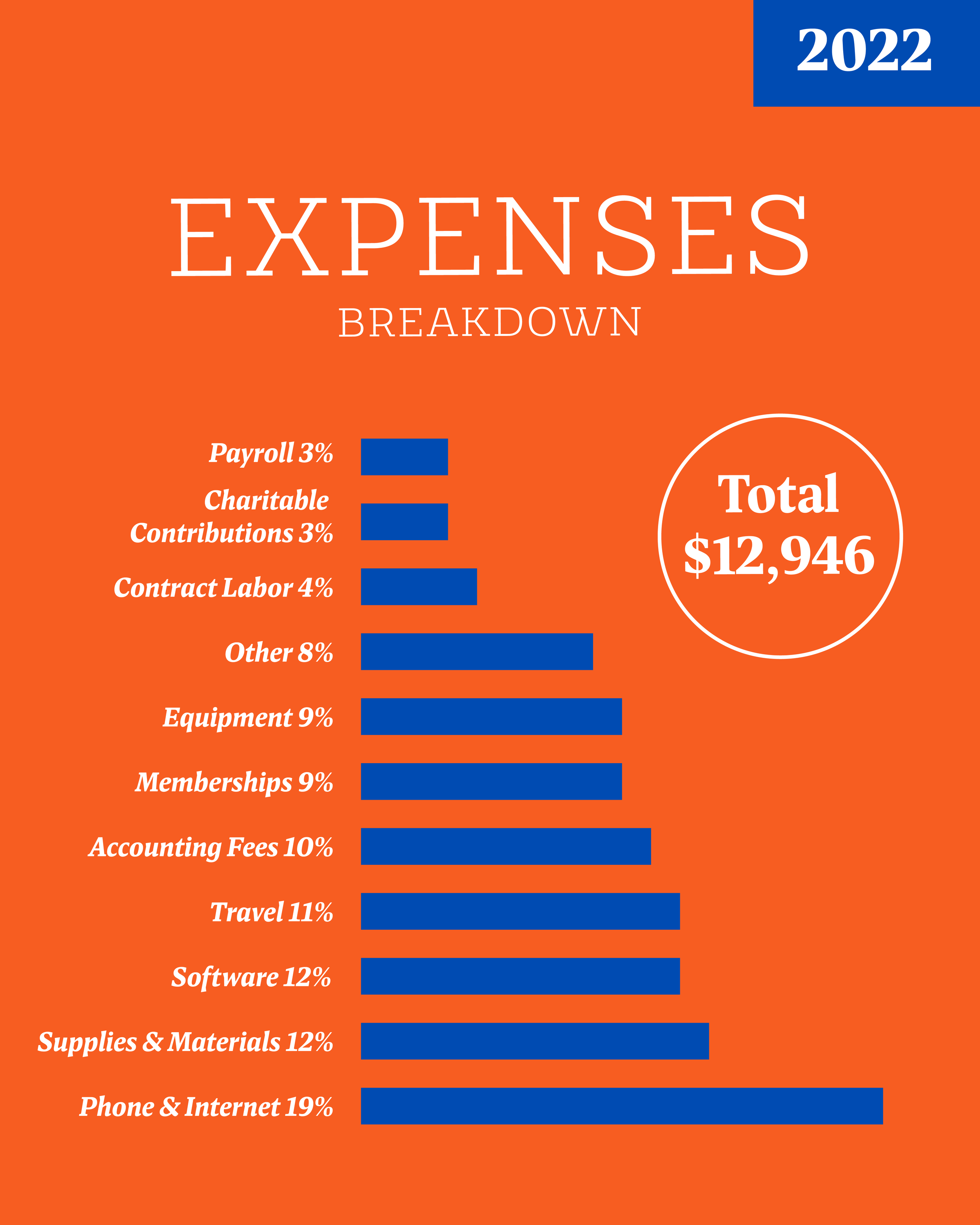

The big news of these two years is that I officially converted Meldel to an S-Corp. To be technical, Meldel is an S-Corp in tax classification only (I still check the LLC box on my W-9 form). What does that even mean?!? An S-Corp allows you to set yourself up as an employee of your own business in the eyes of the taxman. So, now there is Meldel the entity and Melissa Delzio the employee of Meldel. Melissa Delzio the employee now receives a paycheck monthly (ideally) from Meldel. I have the paycheck set up for $2,500 (a modest amount I thought I could always hit monthly). Out of that paycheck comes all the standard taxes that all employees have: federal, state, social security, Medicare, some transit tax I don’t really understand. Last year, added to that list was Paid Leave and OregonSaves (see details below). Anything that’s left drips into the personal bank account that I share with my husband. All the other income I earn counts as earnings for Meldel the entity. All my business expenses get deducted from Meldel income and I am taxed on whatever is leftover. The idea is to reduce the heavy load of self-employment taxes. The upside is less money paid in taxes and in theory a more balanced income. The downsides, are spending more money on accounting fees, paying for and managing a payroll software (Gusto) and bookkeeping (more than my usual spreadsheet output at year’s end). Thanks to Liz at Bean Counter Bookkeeping for getting me up and running on Quickbooks.

I had a rocky start my first two years as

an S-Corp, driven by two mistakes.

I set up the S-Corp in 2021 as a “late election” meaning I wanted it to apply to the full year, even though we set it up in December. The first mistake was when, in the process of setting up my payroll, I had to basically record all the income that Melissa Delzio the employee would have made that year. But, somehow when it all went through, the payroll (for the year’s salary) accidentally posted the date as 1/1/2022. (Insert Janet Leigh’s shower scream face from Psycho). Since I posted nearly a year’s income in the first month of 2022, I basically spent much of my first year as an S-Corp skipping payroll to make up for this giant January infusion. My second mistake which compounded this problem, was when I set up payroll in Gusto, somehow NO federal taxes were set up to be deducted. So, for all of 2022 and part of 2023, Melissa Delzio the employee paid no federal income tax, which of course was revealed in April 2023 when I received a huge tax bill. How could this happen? I set up my payroll system together with my accountant who I was on a call with, screen sharing and somehow these details were missed. I put too much faith in another professional, went on autodrive, and didn’t think critically myself. I should have noticed this mistake in my payroll, but I ran so few of them that year, and there were many other taxes that were taken out, so I missed it. The result was many months of catch up in 2023 to recover from the federal taxes owed. The sea saw has finally leveled out, and it is my goal for 2024 to make and increase Melissa Delzio’s salary so I can funnel more money through my personal return, leaving less to be cleaned up by Meldel.

In the graphics, you will see the disparity in taxes paid between the two years, this is because of this problem outlined above. You will NOT notice the income disparity. That is because I based these income reports on the money that was mark as “PAID” in the calendar year from my invoicing software, Harvest. That is the most accurate reflection of money that came into Meldel, as opposed to income reported for tax purposes (divided across entities). Still reading through that domino of disasters? Now on to some hopeful new programs!

Paid Leave

Being a freelancer sometimes feels like walking a tightrope without a safety net. You are constantly evaluating and finding ways to mitigate risk. What if I become disabled? (Get disability insurance.) What if I get sued? (As an LLC, I have limited liability to protect personal assets.) Health insurance, auto, home and umbrella insurance are also key to ensure personal financial stability. But one gaping benefit that was lacking in my life as a freelancer was paid leave. No more! Starting in January of 2023, the state of Oregon’s Paid Leave program went live, allowing employees to contribute on a monthly basis 1% of their wages to buy into the benefit. Now, you can use the benefit (a percentage of your wages) for any number of scenarios: birth of a child, to care for a family member, to escape domestic violence or for medical leave. The benefit amount is determined by “… a sliding scale using the wages you earned in your base year and the state average weekly wage.” This handy chart breaks down various scenarios. The best part is that this program was designed for self-employed people too, but as a self-employed person, you have to apply to the program and additionally, your weekly benefit amount depends on how long you have been making contributions.

For someone like me, there is an extra layer of confusion/work to do! Since I am now an S-Corp (my own employee and employer) I contribute to Paid Leave through my payroll service, Gusto. Money comes out monthly from Melissa Delzio the employee’s payroll taxes. But, if I were to leave it just as that, when it came time to apply for the benefit, my benefit would be low because it would be based solely on the annual income that I was paid as an employee of Meldel ($30,000). In talking to the lovely customer support people at Oregon Paid Leave, I realized that I also had to sign up as a self-employed person. In applying as a self-employed person, I will have the opportunity to contribute more so that the benefit will consider my full salary! As of this writing, I am in the process of applying for that self-employed benefit, so I hope to have a fuller understanding of my potential benefits within a month. As of now, I am only partially contributing to this, but I should be able to access this full benefit within a year—though I hope I don’t have to. This extra hassle of essentially having to sign up and apply through multiple avenues is inconvenient to say the least. Nevertheless, this is a new program, and I am so grateful I have access at all. Oregon is only the 12th state in the nation with paid family and medical leave for workers, so I sincerely appreciate the lawmakers of the 2019 Oregon legislature for creating this program.

Retirement

Another new program initiated by the state of Oregon is hugely beneficial for independents like me who struggle to set aside money for retirement. Here again, Oregon is a leader. OregonSaves was the first state-based program designed to address the retirement savings crisis when it launched in 2017. The program was rolled out to small businesses in 2023, so I was finally able to take advantage.

OregonSaves is a program that allows self-employed people an easy and automatic way to save money in a Roth IRA. Through my payroll processor, Gusto, I set up OregonSaves to automatically take 10% of my Melissa Delzio employee income and funnel it to an IRA (through Vestwell). Setup for this was also a bit confusing, since again I am both the employee and employer. But with some support, I got this up and running in late 2023. Now I am set to invest $3,000 annually into a target-date 2045 fund automatically through this process! Note, there are limits to what you are allowed to set aside per year depending on income. Target-date funds are diversified funds that automatically rebalance as you get closer to the target retirement date. So again, hats off to the Oregon state legislature (House Bill 2960) for this vital service. When there is much despair around how the government operates, especially at a federal level, it is nice to see progress happening more locally.

Aside from signing up for the OregonSaves program, I have taken advantage of my teaching jobs at PNCA and PSU to use these institutions to help me invest in retirement in a more automated way. Both institutions offer adjunct faculty the ability to have a percentage of their paycheck funneled to retirement accounts, and so I have set this up at both institutions so that about 50% of my teaching income goes straight to these accounts. The accounts contain a few diversified funds, both traditional IRAs and Roth IRAs. While my employers don’t match funds, it is nice to have this process automated so I don’t need to manage monthly contributions on my own! This is reflected in my 2023 retirement contribution numbers, but not in 2022 because I did not have the contributions fully set up for PNCA that year.

The Squeeze

We are still wading through a period of high inflation and economic uncertainty as a country. In Oregon in 2022, inflation rate was measured as 8.1%. We can feel this squeeze in everyday life, with things big and small. The go-to Friday night meal my husband and I order from our local wing joint went up from $35 to $65 in the last three years. My monthly cost for health insurance went from $4,356 annually in 2018 to $7,764 annually in 2023. The consumer price index, states that earning 100,000 a year in 2018 is the equivalent of earning over $123,000 in 2024. Meanwhile, my six-year income has remained rather consistent, hovering on average around 100,000. All this leads to the uneasy feeling of sinking while outwardly feeling successful. I know this feeling is shared, a PBS article from January 2024 states, “Even as inflation in the United States has slowed significantly, [since 2022] overall prices remain nearly 17% above where they were before the pandemic erupted three years ago, which has exasperated many Americans.”

Recently, I rewatched Lauren Greenfield’s documentary, Generation Wealth in which she interrogates materialism, celebrity culture and our exorbitant craving for achieving social status through wealth. In the film, an interview subject says, “We hold out the illusion of the American dream, but not only can we and our children not obtain what generations have before, but things are getting worse. The only social mobility you have is fictitious. The presentation denies your reality.” I do feel there is misalignment between perception of an economy roaring back post-pandemic, and the slow backslide of spending power.

Writing all this has me thinking, no wonder I am exhausted by the freelance hamster wheel! But in deep talks with friends who are gainfully employed at agencies or large corporations, hustle and uncertainty are par for the course in the creative industry in Portland right now. Taking breaks is key. Whiskey helps. And spring flowers. If budgets don’t allow for an elaborate vacation this year, you’ll find me off the clock this summer in my front yard hammock.

I hope this report helps other freelancers, or small business owners in the creative industry and beyond. If you have questions, or want to share an experience or a resource, I would love to hear from you!

- Melissa Delzio

Past reports:

2020-2021 Report

2019 Report

2018 Report

2016 Report

Note: These numbers may not align with numbers from tax filings. This is because I track my personal income for the purpose of this report as money marked as “paid” from my invoicing software in that calendar year. Similarly, this report reflects taxes that were paid by calendar year, not tax year. And for retirement in 2024, I am contributing money that will be attributed towards my 2023 contributions, but it won’t show up here. Don’t come at me IRS!!